Pillsbury SALT attorneys Zachary Atkins, Craig Becker, Carley Roberts, & Richard Nielsen discuss California Assembly Bill 52. AB 52 would provide corporation and personal income tax credits for local sales and use and district taxes paid on machinery and equipment primarily used in manufacturing, research and development, electric power generation or production, or electric power storage and distribution.

Articles Posted in States

New York Administrative Law Judge Holds ITFA Preempts Taxation of Gross Receipts from ADSL and Fiber Broadband Sales

Posted

An administrative law judge with the New York State Division of Tax Appeals held that the federal Internet Tax Freedom Act (ITFA) preempted the imposition of New York franchise tax and a metropolitan transportation business tax (MTA) surcharge on gross receipts from sales of asymmetric digital subscriber line (ADSL) and fiber broadband aggregation and access services (Fiber Broadband).

No Day Off for Buehler: California Sources Gain from Sale of Intangible to Domicile and Denies Other State Tax Credit

Posted

The California Office of Tax Appeals (OTA) held a California resident was not entitled to claim an other state tax credit (OSTC) for taxes paid to Massachusetts because gain from the sale of an LLC membership interest was wholly sourced to the taxpayer’s domicile under California law. Continue Reading ›

The California Office of Tax Appeals (OTA) held a California resident was not entitled to claim an other state tax credit (OSTC) for taxes paid to Massachusetts because gain from the sale of an LLC membership interest was wholly sourced to the taxpayer’s domicile under California law. Continue Reading ›

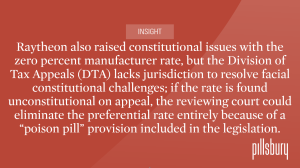

“If You Don’t Make It There, You Can’t Make It Anywhere:” New York’s Zero Manufacturing Rate Requires New York Property

Posted

Our state and local tax team comments on the New York State Division of Tax Appeals (DTA) administrative law judge (ALJ) determination that Raytheon Company and affiliates (Raytheon) did not qualify for New York’s zero percent tax rate for manufacturers or the reduced tax rate for qualified emerging technology companies (QETCs).

Read More: New York’s Zero Manufacturing Rate Requires New York Property (pillsburylaw.com)

Certainly COP: Florida Court Rejects Department of Revenue’s Attempt to Conflate Costs of Performance Sourcing With Market-Based Sourcing

Posted

On March 1, 2023, a Florida trial court confirmed that costs of performance (COP) sourcing, not market-based sourcing, is Florida’s standard methodology for sourcing service receipts for apportionment purposes. In Billmatrix Corp. v. State of Florida, Department of Revenue, No. 2020-CA-000435 (Fla. 2d Cir. Ct. Mar. 1, 2023), the court strongly rebuked the Florida Department of Revenue for attempting to apply market-based sourcing in contravention of its own COP sourcing regulation. Continue Reading ›

On March 1, 2023, a Florida trial court confirmed that costs of performance (COP) sourcing, not market-based sourcing, is Florida’s standard methodology for sourcing service receipts for apportionment purposes. In Billmatrix Corp. v. State of Florida, Department of Revenue, No. 2020-CA-000435 (Fla. 2d Cir. Ct. Mar. 1, 2023), the court strongly rebuked the Florida Department of Revenue for attempting to apply market-based sourcing in contravention of its own COP sourcing regulation. Continue Reading ›

California Lawmakers Propose Constitutional Amendment to Abolish the State Board of Equalization

Posted

California Democratic lawmakers recently introduced Assembly Constitutional Amendment 11 (ACA 11) which proposes to abolish the State Board of Equalization (BOE) and reassign its responsibilities to other state tax agencies effective January 1, 2026. Continue Reading ›

Property Tax Rate Dispute Merits California Supreme Court Review

Posted

For years, some California counties have been imposing disproportionately higher property tax rates on centrally assessed property despite the state constitutional mandate that this property be assessed like locally assessed property.

In a challenge brought by centrally assessed utilities, the California Court of Appeal conceded that the higher property tax rates disproportionally burden utility company property but concluded that this disparity does not violate the California Constitution.

Click here to read the full article.

UPDATE: California Adds New Counties, Further Extends Deadlines to File and Pay Taxes for Businesses and Individuals Affected by Severe Winter Storms

Posted

In addition to the tax relief announced in January, the California Franchise Tax Board (FTB) has automatically extended the income tax filing and payment deadlines for businesses and individuals affected by severe winter storms in California until October 16, 2023.

Texas Comptroller Takes a Serious Look at Sourcing Regulation After SiriusXM Loss

Posted

The Texas Comptroller of Public Accounts has proposed significant amendments to its service receipts sourcing regulation in the wake of the Texas Supreme Court’s decision in Sirius XM Radio, Inc. v. Hegar, 643 S.W.3d 402 (Tex. 2022). The proposed amendments would dispense with the Comptroller’s long-standing “receipts-producing, end-product act” test and align the underlying regulation with the SiriusXM decision.

California Extends Deadlines to File and Pay Taxes for Businesses and Individuals Affected by Severe Winter Storms

Posted

Following the IRS’s announcement of tax relief for 41 California counties* affected by severe winter storms, the California Franchise Tax Board (FTB) and California Department of Tax and Fee Administration (CDTFA) announced similar relief for state-level taxes and fees.