Pillsbury SALT partner Carley Roberts will present during COST’s 52nd Annual Meeting on October 19 in Las Vegas, NV.

Pillsbury SALT partner Carley Roberts will present during COST’s 52nd Annual Meeting on October 19 in Las Vegas, NV.

Pillsbury SALT attorney Jeff Phang will present during CLA’s taxation webinar on September 13. Jeff is partnering with Annie Rothschild (Eversheds Sutherland) to present on the topic, “Recent Developments in California Income Tax Apportionment and Sourcing Law.”

California’s Court of Appeal again held that a special tax measure placed on the local ballot as a citizen initiative required only a simple majority, not a supermajority, vote to pass.

Proposition G is a school parcel tax initiative that passed on San Francisco’s June 2018 ballot with 60.76% of the vote. The Proposition G school parcel tax is a special tax—in other words, the expenditure of its revenues is dedicated to a specific project or projects—and not a general tax, which revenues roll into the locality’s general fund. Here, the Proposition G school parcel tax funds are earmarked for educators’ salaries, staffing, professional development, technology, charter schools, and oversight of funding.

California’s Court of Appeal held a local sales tax ordinance (Measure K) was a general tax, not a special tax, and therefore its adoption did not require a two-thirds vote (supermajority) under California’s Constitution. A tax is “special” and therefore would require a two-thirds vote, when the expenditure of its revenues is dedicated to a specific project or projects. The plaintiffs argued that Measure K was a special tax because the funds were earmarked for the funding of the county’s public safety services and essential services. The Court of Appeal disagreed, concluding tax proceeds that are deposited in a separate account for unspecified “other essential services” could be used for any and all government services that qualify as an “essential service” and are therefore not dedicated to a specific project or purpose, indicative of a general tax. Thus, the court held Measure K was valid.

California’s Court of Appeal held a local sales tax ordinance (Measure K) was a general tax, not a special tax, and therefore its adoption did not require a two-thirds vote (supermajority) under California’s Constitution. A tax is “special” and therefore would require a two-thirds vote, when the expenditure of its revenues is dedicated to a specific project or projects. The plaintiffs argued that Measure K was a special tax because the funds were earmarked for the funding of the county’s public safety services and essential services. The Court of Appeal disagreed, concluding tax proceeds that are deposited in a separate account for unspecified “other essential services” could be used for any and all government services that qualify as an “essential service” and are therefore not dedicated to a specific project or purpose, indicative of a general tax. Thus, the court held Measure K was valid.

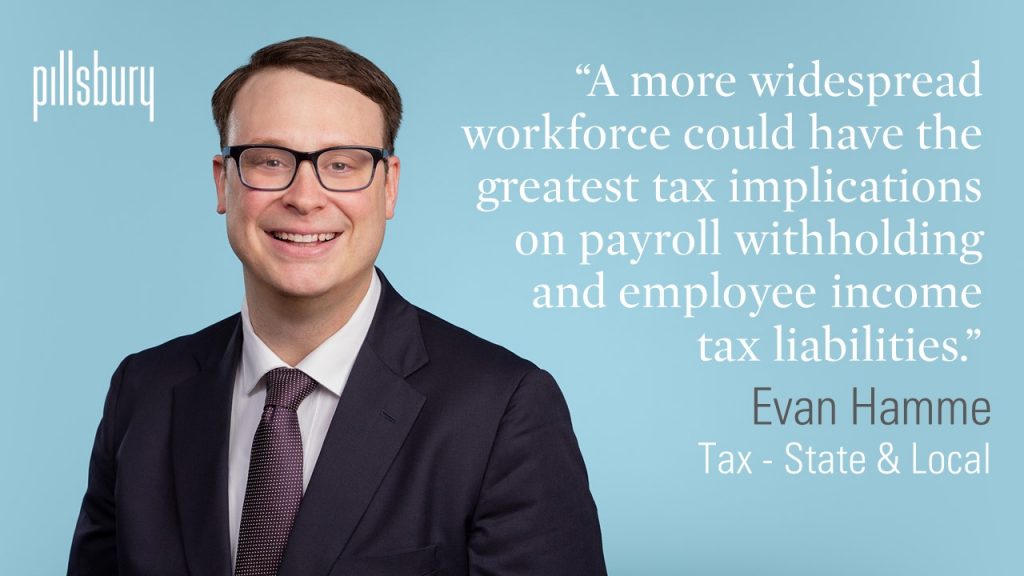

Pillsbury Counsel Evan Hamme discussed how the rise in remote work could lead to tax compliance issues for employers with Law360. Read more here. Continue Reading ›

Continue Reading ›

Pillsbury SALT partner Carley Roberts will participate in the CalTax Webinar series on August 24. The theme for the webinar is “How to Navigate the Appellate Process at the OTA.”![]()

Pillsbury SALT partner Jeffrey Vesely will present during COST’s State Transaction Tax Webinar on July 15. Continue Reading ›

The Massachusetts Supreme Judicial Court recently held that software vendors have a statutory right to apportion tax on the sale of prewritten computer software purchased for use in multiple states and that they may do so through the Commonwealth’s general tax abatement process. The court’s decision in Oracle USA, Inc. v. Commissioner of Revenue, 487 Mass. 518 (2021) confirms that the ability to apportion tax on software is not contingent on strict compliance with the administrative procedures set forth in the Massachusetts Commissioner of Revenue’s apportionment regulation. The tax abatement process is an acceptable mechanism for taxpayers to seek tax apportionment with respect to software purchased for use in multiple jurisdictions. Continue Reading ›

Continue Reading ›

On May 25, the U.S. Solicitor General filed its highly anticipated brief in New Hampshire v. Massachusetts  and recommended that the Court decline jurisdiction over the case. Although the ultimate decision is yet to be issued, the U.S. Supreme Court generally follows the Solicitor General’s recommendations after, as here, the Court requests the U.S. government’s input.

and recommended that the Court decline jurisdiction over the case. Although the ultimate decision is yet to be issued, the U.S. Supreme Court generally follows the Solicitor General’s recommendations after, as here, the Court requests the U.S. government’s input.

Pillsbury attorneys Zachary T. Atkins, Breann E. Robowski, Craig A. Becker, Jay E. Silberg, and Jeffrey S. Merrifield discuss the New York law raising property tax issues and how it could become a national concern in Pratt’s Energy Law Report. Read more here.